This week Gnosis (GNO) price notched a swift 50%+ rally after the project took another step forward in its transition to the Coincidence of Wants Procotol, or CoW, an interface that offers traders protection from miner extracted value (MEV).

Data from Cointelegraph Markets Pro and TradingView shows that the price of GNO has gained 86% over the past seven days, rising from a low of $308 on March 21 to an intraday high at $574 on March 28.

GNO/USDT 4-hour chart. Source: TradingView

Three reasons for the rapid price increase for GNO are the release of the CowSwap (COW) token, which was airdropped to Gnosis holders, traders’ appreciation of the MEV-protection offered by the protocol and the potential for GNO holders to receive additional airdrops in the future.

COW drops!

The most recent price surge appears primarily connected to the official release of COW, the native token of the CowSwap protocol which offers traders MEV-protection.

$COW token is finally expected to unlock around 3pm UTC today.

This will kick off a 12 week $COW liquidity mining program on @ethereum & @gnosis chain aginst $ETH and $GNO pairs.

COW tokens were airdropped to GNO holders based on the number of tokens held or staked during a snapshot that was taken back in early January, with 5% of COW tokens going to GNO holders who could receive an extra 5% if they had locked their GNO tokens on the protocol for a period of one year.

At the time of writing, COW has been listed on Uniswap and is trading at a price of $1.35.

MEV protection features add value to GNO and COW

The main draw of the CowSwap protocol is the MEV-protections offered that can help traders get better terms on swaps and avoid being front run or the victim of a sandwich attack.

What Ethereum people call “Miner Extracted Value” is what Bitcoiners call a game theory fail.

MEV = willfully frontrunning transactions, paying higher fees to do flash loans, sandwich attacks, etc.

It’s a mix between extortion, pickpocketing & perverse free market incentives.

Miner extracted value is a sort of “invisible” tax that occurs on the Ethereum (ETH) network where miners can increase their profitability by including, excluding or re-ordering transactions within the block they produce.

This feature allows miners to conduct certain exploits including front-running, back-running and transaction sandwiching, which help to increase profits at the expense of traders.

Future airdrops could give a long-term boost to GNO price

A third factor helping to boost the demand for GNO is the prospect of additional airdrops coming to GNO holders and stakers.

This includes an allocation of the soon-to-be-released SAFE token for Gnosis Safe, a platform in the Gnosis ecosystem that is designed to securely manage digital assets.

According to data from Dune Analytics, there is currently more than $77 billion worth of value held in Gnosis Safe contracts, a substantial amount that hints at the amount of trust various depositors have in the protocol.

Total USD value of assets stored in Gnosis Safe. Source: Dune Analytics

Documentation released by Gnosis Safe indicates that 20% of SAFE tokens will be distributed to the GNO community via direct distribution to GNO holders and a substantial deposit into the GnosisDAO treasury.

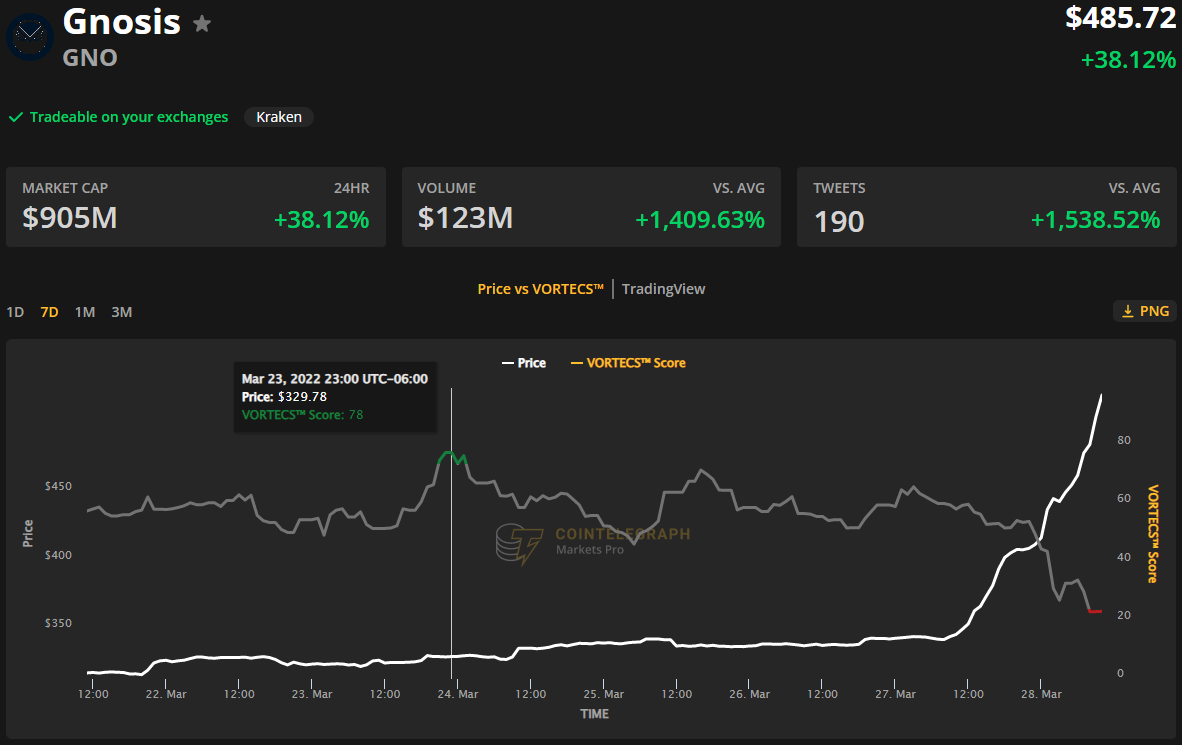

VORTECS™ data from Cointelegraph Markets Pro began to detect a bullish outlook for GNO on March 23, prior to the recent price rise.

The VORTECS™ Score, exclusive to Cointelegraph, is an algorithmic comparison of historical and current market conditions derived from a combination of data points including market sentiment, trading volume, recent price movements and Twitter activity.

VORTECS™ Score (green) vs. GNO price. Source: Cointelegraph Markets Pro

As seen in the chart above, the VORTECS™ Score for GNO began to pick up on March 23 and hit a high of 78 around nine hours before the price increased 78% over the next four days.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph.com. Every investment and trading move involves risk, you should conduct your own research when making a decision.

Bitcoin (BTC) and several altcoins surprised with their newfound strength during the weekend. Bitcoin’s rally easily sliced through the $45,900 level, which according to Glassnode was an area of resistance because several investors had purchased near that level when Bitcoin was declining after hitting its all-time high in November.

Bitcoin’s strength may have attracted buying in several altcoins, which are still languishing below their 52-week high. The rally in Bitcoin and the bottom fishing in altcoins has boosted investor sentiment, pushing the Crypto Fear and Greed Index into the “greed” territory.

Interestingly, the crypto markets have held a large part of their gains despite the tepid performance of the U.S. stock markets on March 28. This suggests that the crypto markets may be in the early stages of decoupling from the equity markets.

Could buyers sustain the momentum and clear the overhead resistance levels? Let’s study the charts of the top-10 cryptocurrencies to find out.

BTC/USDT

Bitcoin hesitated on March 26 as seen from the inside-day candlestick. This indicated indecision among the bulls and the bears. This uncertainty resolved to the upside on March 27 as the bulls regrouped and propelled the price above the overhead resistance at $45,400.

BTC/USDT daily chart. Source: TradingView

The sharp rally of the past few days has pushed the relative strength index (RSI) into the overbought zone for the first time since October 2021. This suggests that the momentum favors the buyers.

The bears may attempt to stall the up-move at the resistance line of the ascending channel but if bulls overcome this barrier, the BTC/USDT pair could rally to the psychological level at $50,000 and later to $52,000.

If the price turns down from the resistance line, the buyers will try to flip $45,400 into support. If they succeed, it will suggest that the up-move may continue. The bears will have to pull and sustain the price below $45,400 to weaken the bullish momentum.

ETH/USDT

Ether (ETH) broke above the symmetrical triangle on March 25 but the bulls could not sustain the higher levels. However, the buyers did not cede ground to the bears and resumed their purchase on March 26.

ETH/USDT daily chart. Source: TradingView

The momentum picked up on March 27 and the ETH/USDT pair has reached $3,411 where the bulls may encounter a minor resistance. If bulls bulldoze their way through, the ETH/USDT pair could rally toward the psychological level at $4,000.

Alternatively, if the price turns down from $3,411, the pair could retest the breakout level from the triangle. If the price rebounds off this level, it will suggest strong buying on dips. The bulls will then again try to resume the up-move.

The bears will have to pull and sustain the price inside the triangle to suggest that the bullish momentum may have weakened.

BNB/USDT

Binance Coin (BNB) continued its northward march and has reached the overhead resistance at $445. The bears are likely to defend this level with vigor.

BNB/USDT daily chart. Source: TradingView

The rising 20-day exponential moving average ($402) and the RSI near the overbought zone indicate that bulls are in control. If buyers thrust the price above $445, the BNB/USDT pair could rally toward the psychological level at $500. This level could again act as a strong resistance.

If the price turns down from $500 but does not break below $445, it will suggest that the bulls have flipped the level into support. That will increase the likelihood of a break above the overhead resistance.

Contrary to this assumption, if the price turns down from $445, the pair could drop to the 20-day EMA.

XRP/USDT

XRP turned up on March 26, indicating that bulls are buying on minor dips. The buyers pushed the price above the strong resistance at $0.86 but are facing resistance near $0.91.

XRP/USDT daily chart. Source: TradingView

Both moving averages are sloping up and the RSI is in the positive zone. If buyers do not allow the price to slide below $0.86, the prospects of a break above $0.91 increase. If that happens, the XRP/USDT pair could rally to the psychological level at $1.

This positive view will be invalidated if the price turns down from the current level or the overhead resistance at $0.91 and plummets below the moving averages. Such a move could pull the price to the strong support at $0.70.

ADA/USDT

Cardano (ADA) has continued its recovery and the price has reached the overhead resistance at $1.26 where the bears are likely to mount a strong defense.

ADA/USDT daily chart. Source: TradingView

The rising 20-day EMA ($1) and the RSI in the overbought zone suggest that bulls are in control. If the price turns down from overhead resistance but the bulls do not give up much ground, it will increase the possibility of a break above $1.26.

If that happens, the ADA/USDT pair could rally to $1.60 and then march higher toward $1.80. This bullish view will invalidate if the price turns down from the overhead resistance and breaks below the psychological level at $1.

LUNA/USDT

Terra’s LUNA token has been stuck in a tight range between the overhead resistance at $96 and the support at the 20-day EMA ($90). This tight-range trading could soon lead to a sharp trending move.

LUNA/USDT daily chart. Source: TradingView

The rising 20-day EMA and the RSI in the positive territory suggest that the path of least resistance is to the upside. If buyers propel and sustain the price above $96, the LUNA/USDT pair could retest the all-time high at $105.

This level is likely to act as a major obstacle but if bulls overcome it, the uptrend may resume. The pair could then rally to $125. This positive view will invalidate in the short term if the price turns down and breaks below the 20-day EMA. That could open the gates for a possible decline to $82.

SOL/USDT

After trading near the overhead resistance at $106 for a few days, Solana (SOL) broke and closed above the level on March 27. The moving averages have completed a bullish crossover and the RSI is near the overbought zone, indicating advantage to buyers.

SOL/USDT daily chart. Source: TradingView

If bulls sustain the price above $106, the SOL/USDT pair could rise to $122. The bears are expected to defend this level aggressively. If the price turns down from this level and breaks below $106, it will suggest that the pair may remain range-bound for a few more days.

The bulls will have to clear the overhead hurdle at $122 to signal the start of a new potential uptrend. The pair could then start its up-move which could reach the overhead resistance zone between $158 and $163.

Avalanche (AVAX) rebounded off the 20-day EMA ($83) on March 26, indicating that bulls are buying on dips. The buyers will now try to sustain the price above the immediate resistance at $92.

AVAX/USDT daily chart. Source: TradingView

If they succeed, the AVAX/USDT pair could rally to the overhead resistance zone at $98 to $100. This is an important zone for the bears to defend because a break and close above it could extend the rally to $120.

If the price turns down from the overhead zone, the bears will try to pull the pair to the moving averages. If the price rebounds off this level, the pair may remain stuck between the moving averages and the overhead zone for a few days.

DOT/USDT

Polkadot (DOT) picked up momentum on March 27 and has reached the stiff overhead resistance at $23. The upsloping 20-day EMA ($20) and the RSI near the overbought zone suggest that bulls have the upper hand.

DOT/USDT daily chart. Source: TradingView

If bulls drive and sustain the price above $23, the DOT/USDT pair could rally to $28. If bulls succeed in clearing this hurdle, the up-move may extend to $30 and later to $32.

Alternatively, if the price turns down from the overhead resistance, the bears will try to pull the pair to the 20-day EMA. A strong rebound off this support will suggest that bulls continue to buy on dips. That will increase the possibility of a break above the overhead barrier.

This positive view will invalidate if the price breaks below the moving averages. That could extend the consolidation between $16 and $23 for a few more days.

DOGE/USDT

The bulls flipped the 50-day simple moving average ($0.13) into support on March 25. This attracted strong buying in Dogecoin (DOGE), putting it on the path for a possible rally to $0.17.

DOGE/USDT daily chart. Source: TradingView

The moving averages are on the verge of a bullish crossover and the RSI is near the overbought zone, indicating that buyers have the upper hand. If bulls drive the price above $0.17, the DOGE/USDT pair could rise to $0.22.

If the price turns down from $0.17 but does not give up much ground, it will suggest that the traders expect the recovery to continue.

Conversely, if the price turns down sharply from the current level or the overhead resistance, it will signal that the pair may remain range-bound between $0.12 and $0.17 for a few more days.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.

Cointelegraph is following the development of an entirely new blockchain from inception to the mainnet and beyond through its series, Inside the Blockchain Developer’s Mind, written by Andrew Levine of Koinos Group.

Scalability is a popular topic in blockchain, but few ever explain what we mean by that term. When we at Koinos Group talk about scaling what we mean is scaling to the masses. Creating a blockchain that everyone on Earth can use. That means the blockchain network has to be able to support that level of load, which is typically what people mean when they refer to scalability.

User experience matters

But what they talk about far less is the obvious implication that you must have a user experience that everyone on Earth can find pleasurable. Terrible user experiences are infinitely scalable because there is no demand for bad user experiences and the underlying network resources required to deliver them.

This is demonstrated by the fact that when most projects talk about scaling, they talk about technical implementations like sharding, proof-of-history, or layer 2, which are the solutions that Ethereum is using to solve its scaling challenges.

These projects are responding to Ethereum’s scaling constraints by trying to integrate those scaling solutions sooner, but are failing to realize that those solutions only make sense in Ethereum’s context as not only the first general-purpose blockchain but the one with the most developer adoption in the world.

Ethereum: The first mover

When Ethereum was released, it gave developers, for the first time ever, the ability to develop applications on a shared blockchain platform using a programming language very similar to the ones they were already using to build applications; a Turing complete programming language. Compared to the developer experience of building applications on other blockchains, building on Ethereum was a quantum leap that made it faster, easier and cheaper to build decentralized applications. Thanks to this unparalleled user experience, the usage of Ethereum grew at a high rate. Demand for Ethereum’s resources has outstripped supply, which has led to an increase in demand for gas, and a corresponding price increase, making all Ether (ETH) holders very happy.

The Ethereum developers and stakeholders do not want to eliminate fees or even necessarily reduce them. That would be like oil producers wanting to reduce the price of oil. If there is surplus demand for their network resources, they don’t care about creating a better user experience, they care about increasing supply (scaling) while maintaining the existing user experience.

But that is Ethereum! The 900-pound gorilla of general-purpose blockchains with first mover advantage, incredible developer adoption and unfathomable capital investment. It is a successful platform and its plans for scaling make perfect sense for Ethereum. But they make no sense for platforms that have no usage and no developer adoption.

This is why we see so many projects pursuing labor intensive and risky efforts like bridges to Ethereum in an attempt to siphon users off of Ethereum to trigger the growth they need to justify their scaling solutions!

Reasoning from analogy

But this is classic reasoning from analogy as opposed to reasoning from first principles; making decisions based on what everyone else is doing instead of focusing on the problem you want to solve and the most efficient path for developing a solution based on fundamental truths. Thinking that the way to scale a new blockchain is sharding because sharding is the way to scale Ethereum is a perfect example of reasoning from analogy.

At Koinos Group, we’re approaching this problem from first principles. Scaling to the masses is not about integrating some magical technology that overnight supports everyone and their mother. No technology platform ever goes from zero users to mass adoption overnight. Every platform or product that reaches mainstream adoption only ever achieved that through exponential growth. I’ll repeat that. Every product or platform reaches mass adoption through exponential growth.

What that means is that it doesn’t matter how many users or how many transactions your platform or application stack can handle on Day One. That is effectively irrelevant.

What matters the most is that your product has some unique value proposition that a small number of early adopters will love, even if the cost is relatively high. Koinos allows people to use decentralized applications for free simply by holding liquid KOIN tokens in their wallets. They don’t have to buy an account or consciously stake their tokens because every liquid KOIN token contains mana that is consumed down when they use the blockchain. As an account’s mana gets consumed, the tokens containing that mana are automatically locked for some time, creating an opportunity cost instead of an explicit fee.

Video game experience

This gives the blockchain a video game-like user experience, instead of the unpleasant UX of every other blockchain. This delivers a fundamentally different, and more pleasant user experience, but it’s not like the whole world is going to want to use Koinos on Day One. Ethereum’s fee-based model is still the dominant paradigm, which is only validated by its many imitators/competitors. It also has an army of developers, token holders and institutional investors advocating for it (and by extension, its fee-based model).

On Day One, a relatively small group (hopefully, not too small) of early adopters looking for the next best thing will begin using Koinos. The mainnet needs to be able to give those people a pleasant user experience, but no more. As those people use the blockchain and discover that it truly has a delightful user experience, they will spread the word, and usage of the blockchain will go up.

At a certain point, the usage of Koinos will get high enough that the amount of a user’s tokens getting locked is very high and the new user experience relative to the original user experience might be unacceptable. This is what Koinos hitting its scaling constraints looks like. But bear in mind, the user is still not losing those tokens forever (a fee), they are only sacrificing some opportunity cost, which is an infinitely better user experience.

Upgradeability: The ultimate scaling solution

Koinos has to be engineered so that as adoption grows, the right scaling technologies can be integrated at the right time. This is why Koinos is not optimized for any particular scaling solution, but upgradeability in general, making it as easy as possible for new technologies to be added once they have been sufficiently battle-tested. This turns all of the other projects experimenting with scaling technologies prematurely into fertile testing grounds for Koinos!

Scaling is not an end goal, it’s a process that unfolds throughout the lifetime of a platform, at least, if the platform is sufficiently upgradeable. If the platform isn’t sufficiently upgradeable then you have to pick the “right” scaling solutions on Day One, even if you don’t need it, but this is more of a reflection of poor upgradeability (and bad engineering) than anything else.

This is why I like to say that upgradeability is the ultimate scaling solution.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision.

The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.

Andrew Levine is the CEO of Koinos Group, a team of industry veterans accelerating decentralization through accessible blockchain technology. Their foundational product is Koinos, a feeless and infinitely upgradeable blockchain with universal language support.

The Brazilian city of Rio de Janeiro will officially start accepting Bitcoin (BTC) payments for taxes related to urban real estate within their city limits, a.k.a. Imposto sobre a propriedade predial e territorial urbana (IPTU).

As reported by Cointelegraph Brazil, the new pro-crypto tax laws will be implemented from 2023, which was announced by the Secretary of Economic Development, Innovation and Simplification, Chicão Bulhões.

Supporting this cause led by the Brazilian Mayor Eduardo Paes, Binance CEO Changpeng Zhao announced to open a new office in the region stating that “He’s done his part. We are working on ours.”

9 days ago, I made a handshake deal with mayor @eduardopaes. Rio De Janeiro will accept crypto for tax payments, and @Binance will open an office in Rio. He’s done his part. We are working on ours. https://t.co/HPJONtBfQ8

The rollout of this initiative will place Rio de Janeiro as the first Brazilian city to mainstream BTC payments. According to the translated announcement:

“To enable the operation, the municipality will hire companies specialized in converting crypto assets into reais. In this way, the City Hall will receive 100% of the amount in the currency.”

Brazilian secretary Pedro Paulo further acknowledged that the city’s goal — with the acceptance of cryptocurrencies — is to develop a solid market of this new asset class in the city, adding:

“We will stimulate the circulation of cryptocurrencies by integrating them into the payment of taxes, as in the case of IPTU and, in the future, this can be expanded to services such as taxi races, for example.”

The city also plans to involve nonfungible tokens (NFT)-based governance policies across various markets including arts, culture and tourism.

Earlier this year on Jan. 29, Meta, the world’s biggest social media platform, filed a trademark registration with the Brazilian authorities to design, develop and provision hardware and software for various BTC and crypto-related services.

Meta’s trademark filing with the Brazilian INMI. Source: INPI

As Cointelegraph reported, Meta’s trademark filing order was placed on Oct. 5, 2021, from Jamaica.

Filling multiple needs within the cryptocurrency community is one way a project can set itself apart from the competition and new attract users and liquidity to its ecosystem.

Loopring aims to do exactly this by aiming to offer a EVM-based solution with low fees where DeFi and NFT developers and investors can transact. The layer-two (L2) scaling solution utilizes zk-Rollups to provide fast, low-cost transactions and the project has been gaining traction throughout the month of March.

Data from Cointelegraph Markets Pro and TradingView shows that the price of LRC gained 57% between March 21 and March 23 as its price increased from $0.78 to $1.23 amidst a spike in its 24-hour trading volume to $2.75 billion.

LRC/USDT 4-hour chart. Source: TradingView

Three developments that have helped spark the reversal in price for LRC include the beta launch of the GameStop NFT marketplace on the Loopring network, the inflow of new users and a rapidly expanding NFT ecosystem.

GameStop selects Loopring for its upcoming NFT Marketplace

The most significant recent development that helped to drive the increase in demand for LRC was the March 23 announcement that GameStop has integrated the beta version of its NFT marketplace with the Loopring network.

The future of #NFTs are here + they’re powered by #Ethereum‘s second layer

GameStop reports that it chose Loopring to host its NFT marketplace due to the network’s ability to mint NFTs for a fraction of the cost required on Ethereum, with the average fee being less than $1.

Beta users can begin exploring the marketplace now and deposit funds in preparation for the platform’s full lauch which is expected to take place in the near future.

Surging user growth

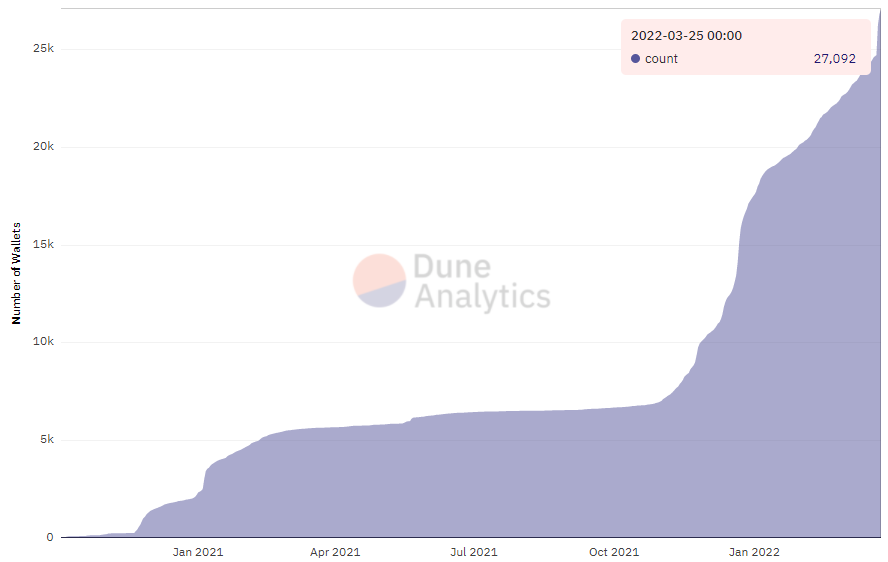

A second factor putting wind in the sails of LRC has been the surge in new users in the Loopring ecosystem as evidenced by the record-high number of wallets joining the netw.

Total number of Loopring wallets. Source: Dune Analytics

According to data from Dune Analytics, the wallet count of the Loopring network has increased from 6,498 on Oct. 30, 2021 to an all-time high of 27,092 on March 25 as the GameStop announcement helped initiate a new of wave users.

The recent release of the Loopring Smart Wallet, which includes the ability to mint NFTs and retrieve a lost account via social recovery and Guardians, has also helped in the process of onboarding new users and wallets in the ecosystem.

A third factor helping to boost the outlook of LRC is the overall growth of its ecosystem which includes a NFT community that has already seen more than 1 million NFTs minted.

Over 1 Million NFTs have been minted on Loopring L2 since the launch of open #NFT minting less than a month ago

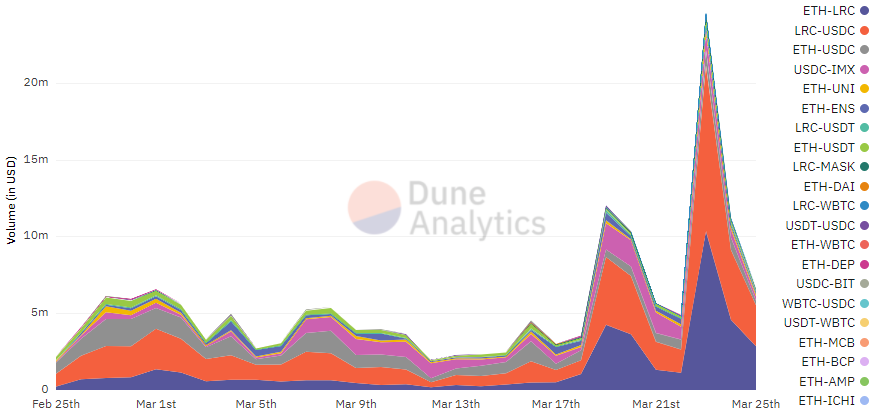

Further evidence of its growth can be found looking at the daily volume traded on Loopring, which experienced a significant spike in activity following the March 23 GameStop announcement.

Loopring volume traded per pair per day. Source: Dune Analytics

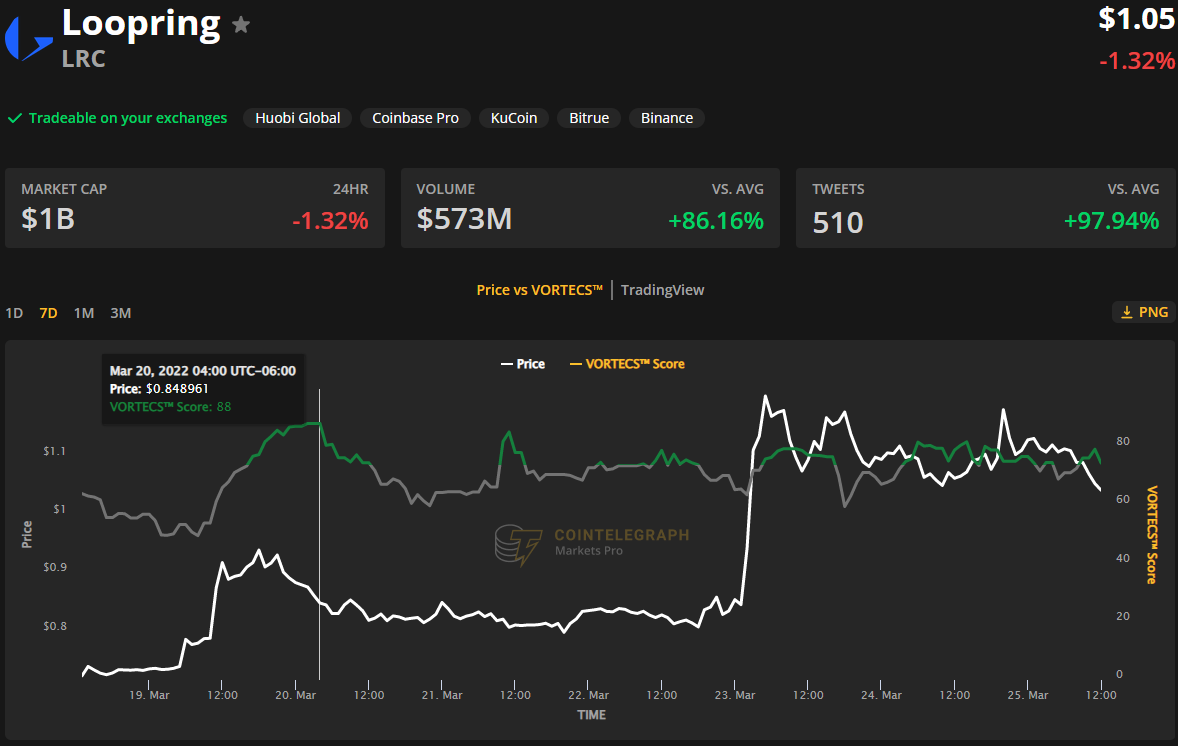

VORTECS™ data from Cointelegraph Markets Pro began to detect a bullish outlook for LRC on March 20, prior to the recent price rise.

The VORTECS™ Score, exclusive to Cointelegraph, is an algorithmic comparison of historical and current market conditions derived from a combination of data points including market sentiment, trading volume, recent price movements and Twitter activity.

As seen in the chart above, the VORTECS™ Score for LRC climbed into the green zone on March 19 and proceeded to hit a high of 88 on March 20, around 40 hours before the price increased 57% over the next two days.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph.com. Every investment and trading move involves risk, you should conduct your own research when making a decision.

Citing compliance with local jurisdictions, crypto exchange Coinbase announced to soon collect additional information from users based in Canada, Singapore and Japan.

Effective from April 1, Coinbase users from Canada, Singapore and Japan will be required to provide additional information while sending cryptocurrencies to a different (non-Coinbase) platform.

However, while Singaporean and Japanese investors will be required to share additional information about the recipient for every single off-platform transaction, Canadians sending less than $801 (1,000 CAD) will be exempted from this requirement.

Screenshot of Coinbase requesting recipient information from Canadian users. Source: Coinbase

As shown in the above screenshot, Canadian users will need to share the full name and residential address of the recipient.

Moreover, Canadian users — that suffice the above two conditions — will lawfully require to provide the recipient’s (self) information even while transferring funds between their own crypto wallets.

On the other hand, both Japanese and Singaporean regulations will require Coinbase to collect information about the recipients from local investors for every single off-platform transaction with no minimum threshold.

Screenshot of Coinbase requesting recipient information from Singaporean users. Source: Coinbase

Similar to Canadian users, investors from Japan will need to disclose information including the recipient’s name and full address and the name of the crypto exchange handling the wallet.

Singapore users will not require to provide the recipient’s residential address but will require only the recipient’s name and country of residence. The lack of any required information will bar the user from sending cryptocurrencies out of the Coinbase platform for the jurisdictions in question.

Coinbase users that no longer reside in these jurisdictions will need to update their country of registration in order to gain exemption from the soon-to-be-implemented rule.

For many jurisdictions, the road to mainstream crypto adoption is paved by stringent regulations under the pretext of investor protection. Starting April 2022, the Thailand Securities and Exchange Commission (SEC) announced a ban on crypto payments throughout the country.

Complementing this law, the SEC also proposed a new rule, which if implemented, will require Thai-based crypto businesses — brokers, exchanges and dealers — to disclose service quality and IT usage information.

As Cointelegraph reported, a joint study between the Thai SEC and Bank of Thailand (BOT) concluded that:

“[Crypto payments] may affect the stability of the financial system and overall economic system including risks to people and businesses.”

Cryptocurrency exchange Crypto.com plans to use its ad time during the 94th Academy Awards on Sunday to air a TV spot regarding the humanitarian crisis in Ukraine.

In a Wednesday announcement, Crypto.com CEO Kris Marszalek said the exchange had partnered with the International Committee of the Red Cross, or ICRC, to launch a campaign aimed at helping those suffering under war-torn conditions in Ukraine. The CEO did not specify what the campaign would entail, but the platform already allows donations in crypto, fiat, and nonfungible token purchases to the humanitarian network Red Cross Red Crescent. The exchange will match up to $1 million in donations until March 31.

“The humanitarian crisis caused by the conflict in Ukraine continues to escalate, and I believe it’s our responsibility to support those in need,” said Marszalek. “Throughout this tragedy, the entire cryptocurrency community has come together to show the world who we are, our values, and the importance of what we’re building.”

We’re matching donations to the Red Cross Red Crescent all weekend, in support of people affected by the crisis in #Ukraine.

According to the ICRC, more than 3.6 million people have fled Ukraine as of March 24, a month since Russian military forces invaded the country. Reports out of Ukraine suggest millions of people are facing food and water shortages, lack of medical care due to many hospitals being damaged or destroyed, and displacement after being forced to leave eastern parts of the country.

Many private businesses are facilitating donations of digital assets including Bitcoin (BTC) and Ether (ETH) towards helping Ukrainians. In addition to Ukraine’s government accepting crypto donations directly through wallet addresses provided by the Ministry of Digital Transformation, the legislative body partnered with exchanges FTX and Kuna and staking platform Everstake to launch a donation website on March 14. Cointelegraph reported that as of March 9, many charities, relief organizations, and government wallets had received roughly $108 million in crypto towards helping Ukraine.

In addition to its efforts for Ukraine, Crypto.com announced on Tuesday it would be an official sponsor of the 2022 FIFA World Cup in Qatar scheduled to begin in November. The exchange has made a major marketing push in the last year, partnering with many sports organizations including the Australia Football League, Formula 1, and Ultimate Fighting Championship.

South Korean tech giant LG Electronics has officially added blockchain and cryptocurrency as new business areas in its corporate charter.

According to a local South Korean news report, LG added two distinct crypto-related objectives during its annual general meeting on Thursday, March 24. The objectives include “the development and selling of blockchain-based software” and “the sale and brokerage of cryptocurrency,” which led to conjecture whether LG would establish some form of crypto exchange.

When asked about the company’s intention to start its own exchange or platform, an LG spokesperson tempered any speculation, stating, “Nothing has been decided yet. We just mentioned business areas in a broad manner.”

Rumors concerning LG creating a crypto-related marketplace emerged earlier this year when Bithumb CEO Heo Baek-young confirmed that the exchange was working with “a large company” to develop an NFT marketplace.

The tech manufacturer has been on a warpath of NFT adoption and integration, announcing earlier this month that it was working with blockchain tech company Kakao’s Ground X to introduce a line of smart TVs that are fully NFT-capable. LG also announced a partnership with Seoul Auction Blue, an online art auctioneer to carry out further projects related to NFT-based artworks.

LG’s announcements come as fellow tech giants and South Korea, more broadly, continue to adopt cryptocurrencies and blockchain-related tech. Earlier this year, fellow South Korean tech giant Samsung, announced that it would be launching an NFT platform for its smart TVs as well as launching its own store in the Decentraland metaverse.

Most notably, the country elected crypto-friendly President Yoon Suk-yeol earlier this month, with Yoon’s election campaign being centered around deregulating South Korea’s crypto industry as well as establishing initiatives to make the country a future home of blockchain technology “unicorns.”

Bitcoin (BTC) and the broader cryptocurrency market rallied on Thursday, as the total value of digital assets crossed $2 trillion for the first time in over three weeks amid signs of a clear shift in market sentiment — headlined by Goldman Sachs, no less.

BTC printed an intraday high of $44,253, having gained more than 3% during the session, according to data from Cointelegraph Markets Pro and TradingView. The largest cryptocurrency by market capitalization has now recovered over 33% from its January low.

The total crypto market cap has gained over 7% since Monday to reach nearly $2.1 trillion, according to Coingecko data. The market capitalization figure also reached $2 trillion on CoinMarketCap.

While not bullish, Bitcoin’s Fear & Greed Index has escaped “extreme fear” and is now in the “fear” stage with a reading of 40. The volatility and sentiment indicator is based on a scale of 0 to 100 with higher readings corresponding to a more bullish outlook for BTC.

Bitcoin’s Fear & Greed Index remains an important proxy for overall market conditions. Source: Alternative.me

The crypto market’s apparent shift in sentiment follows months of downward price action for Bitcoin and altcoins, which led some investors to speculate about the possibility of a full-fledged bear market. Amid geopolitical unrest, however, members of the legacy finance community have identified crypto as a potential opportunity.

As Cointelegraph reported, BlackRock CEO Larry Fink said the war in Ukraine could force nations to reevaluate their currency dependencies, potentially paving the way for digital assets. Specifically, the BlackRock CEO touted digital assets as a viable tool for international settlements and transactions.

Crypto has been on Fink’s radar since at least the fourth quarter of 2020.

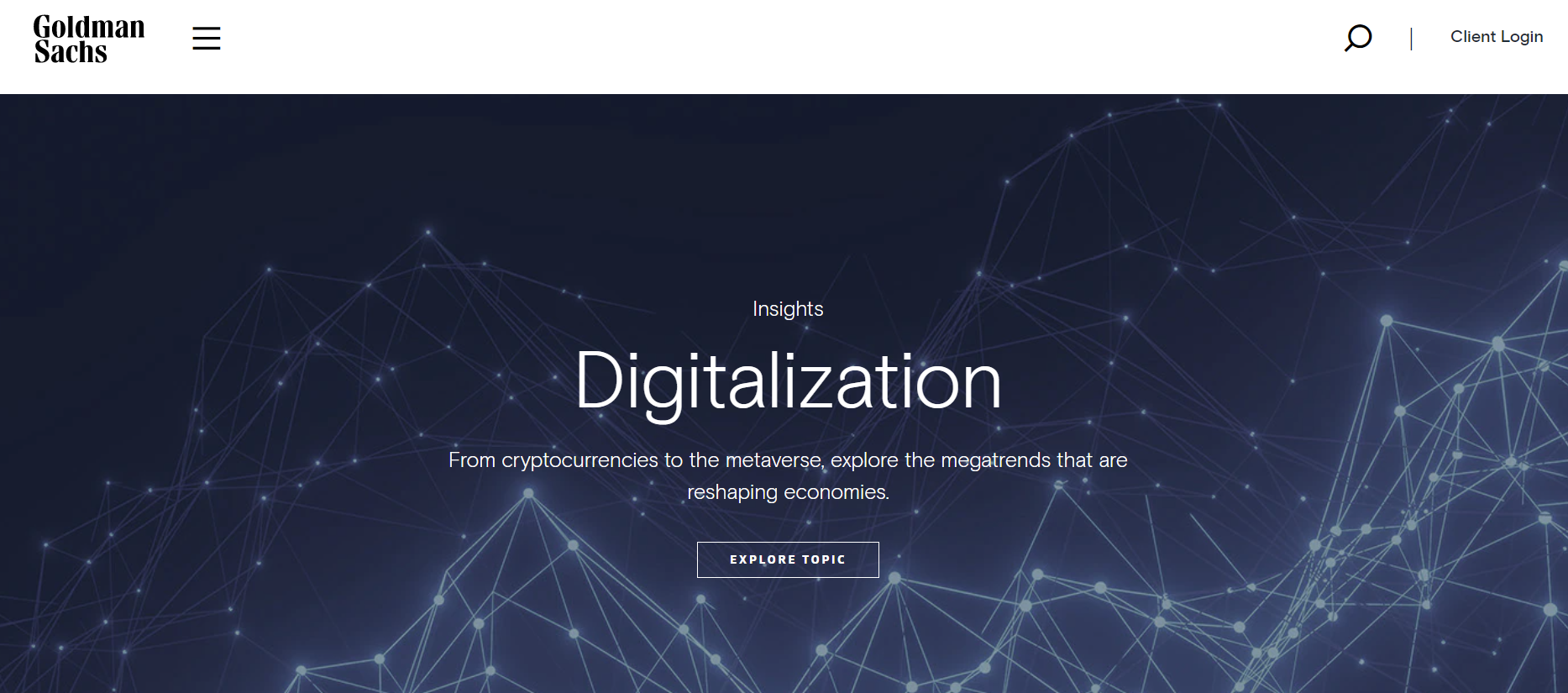

Meanwhile, multinational investment bank Goldman Sachs appears to have put crypto on its radar and even redesigned its website’s homepage to reflect the growth of digital assets and the metaverse. Referring to these technologies as “megatrends,” Goldman populated a new “Insights” section of its website with previously released reports on gaming, the metaverse and Web3.

Goldman Sachs’ homepage on March 24, 2022.

Goldman Sachs recently completed its first over-the-counter crypto options trade with Galaxy Digital. The investment bank first launched its Bitcoin futures product for CME in June 2021.

Finally, Grayscale Investments recently announced the launch of a new smart contract fund that allows accredited investors to back Ethereum competitors. The new fund, which has already opened for daily subscriptions, provides exposure to Cardano (ADA), Solana (SOL), Avalanche (AVAX), Polkadot (DOT), Polygon (MATIC), Algorand (ALGO) and Stellar (XLM).

Stargate Finance, a cross-chain protocol designed to assist users in transferring assets between different blockchains, has accrued over $1.9 billion in total value locked (TVL) in less than a week after launching.

Stargate markets itself as a liquidity transport protocol that allows users to transact native assets cross-chain, offering decentralized finance (DeFi) users the option of staking stablecoins in pools where they are paid out in the native Stargate token (STG).

The rapidly growing TVL is probably down to the “up to 26% APY” being offered farming stablecoin deposits.

By attracting nearly $2 billion in TVL at the time of writing, Stargate has cemented itself as one of the top 10 DeFi projects, according to comparative data from DeFi Pulse.

Stargate has a high-profile supporter in quantitative crypto trading firm Alameda Research CEO Sam Trabucco.

In a Twitter thread to his 150,000 followers, Trabucco announced that Alameda Research had purchased all available Stargate tokens (STG) that were auctioned off during Stargate’s launch on March 17.

There’s been some chatter about the recent @StargateFinance auction, and I wanted to clarify a few things about Alameda’s involvement.

According to LayerZero, the protocol that Stargate runs on, 10% of the total supply of STG or 100 million tokens, were auctioned off to generate liquidity across the seven blockchains that Stargate is launching on.

LayerZero protocol markets itself as an “Interoperability protocol that actually works”.

According to a blog post from LayerZero Labs Co-founder and CTO, Ryan Zarick, the Stargate protocol solves something known as the “Bridging Trilemma” by using unified liquidity pools between chains, instant guaranteed finality of transactions and the use of native assets for cross-chain swaps.

Stargate plans to make it possible for any user to transfer assets from one blockchain to another one in a single transaction, skipping over the need for using complicated and convoluted methods such as locking, minting and burning and redeeming assets.

The LayerZero team also announced that they had hired Maki, the co-founder of SushiSwap, to lead business development at Stargate.

Stargate is currently live on seven primary chains including Ethereum, Polygon, Avalanche, BSC, Fantom, Optimism and Arbitrum. The LayerZero team plans to add support for other chains like Solana, Terra and Cosmos.

price rallies 50%+ after CowSwap users claim COW airdrop")

price surges by 50% after GameStop NFT marketplace integration")